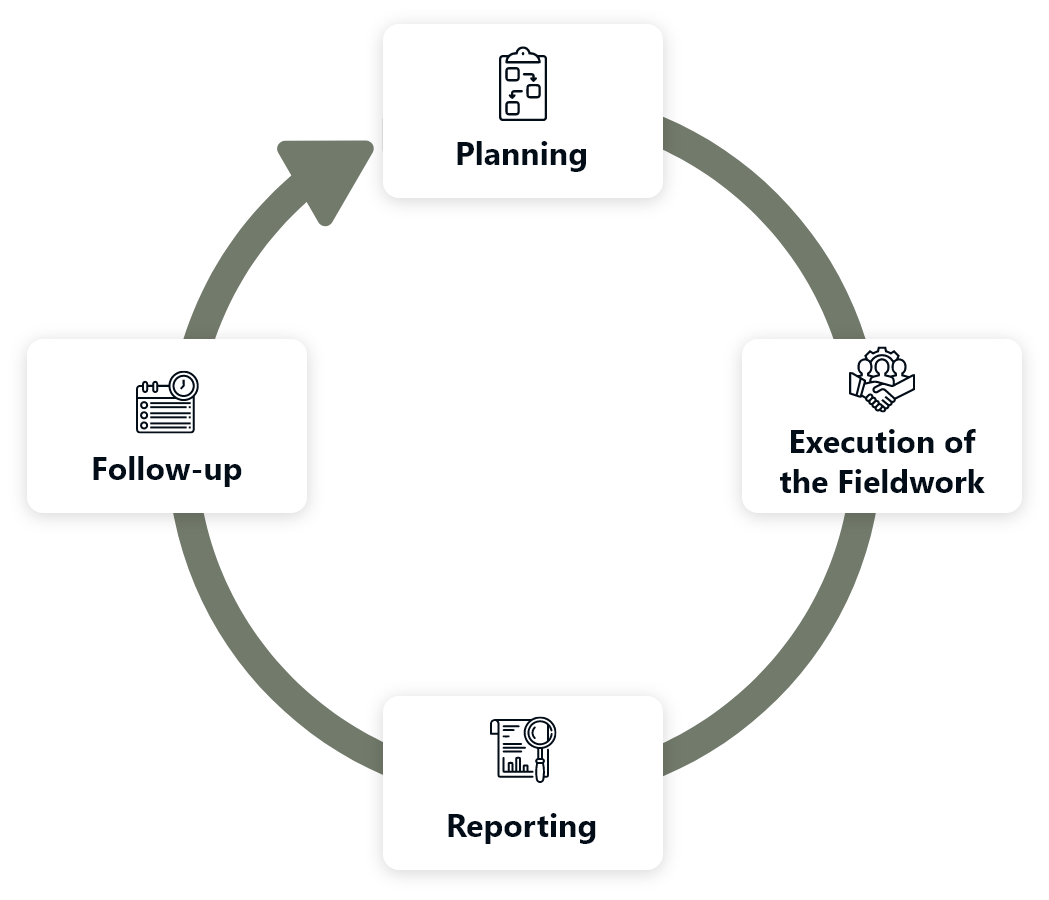

Our audit approach

The Auditor General’s Department utilizes a risk-based approach to determine independently and objectively the nature and extent of the audit that needs to be carried out. The approach requires that auditors have integrated knowledge of the entity and its environment they are assigned allowing for the identification of risks to aid in determining the approach that would be more suitable for the audit.

LinkedIn

LinkedIn Twitter

Twitter Youtube

Youtube